For small and mid-sized employers, the choice between a fully-insured and a level-funded health plan is one of the most consequential — and most misunderstood — decisions in benefits. After 25 years advising groups of every size, I've seen employers overpay for years simply because no one walked them through the difference. Here's the plain-language version.

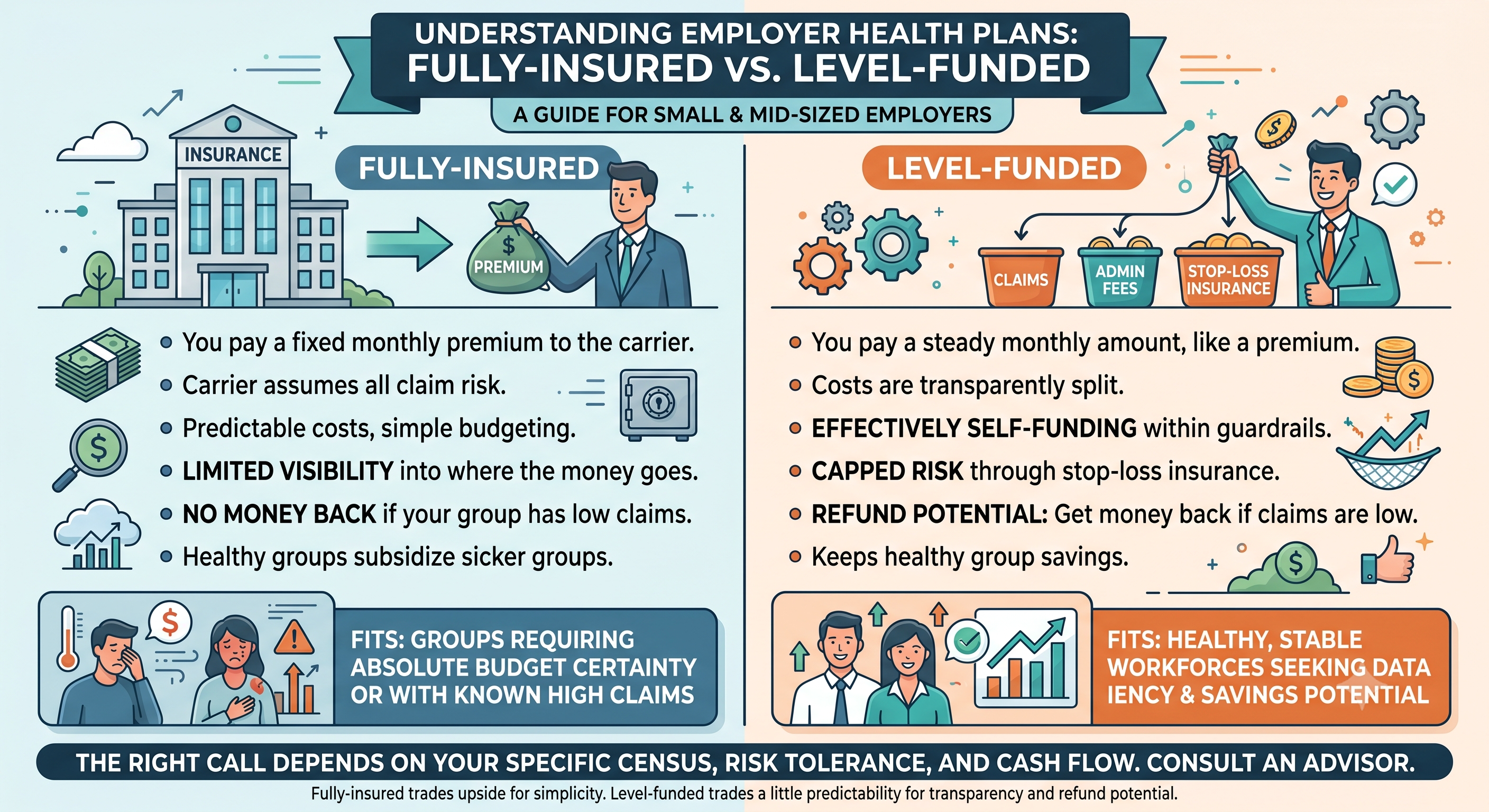

What fully-insured means

You pay a fixed premium to a carrier, and the carrier takes on all the risk. If your employees have a high-claims year, that's the carrier's problem. It's predictable and simple — but you never get money back if your group is healthy, and you have little visibility into where the money goes.

What level-funded means

You pay a steady monthly amount, like a premium, but it's split into pieces: expected claims, administrative costs, and stop-loss insurance that caps your risk. The key difference: if your group's claims come in low, you can get money back. You're effectively self-funding within guardrails.

Why level-funding appeals to healthy groups

A group with a relatively young, healthy workforce often subsidizes sicker groups in the fully-insured pool. Level-funding lets that healthy group keep the savings instead of handing them to the carrier. For the right group, the refund potential is real money.

The risk to understand

Level-funding isn't free of downside. In a high-claims year you may pay more than the fully-insured equivalent — up to the stop-loss cap. The cap protects you from catastrophe, but the monthly predictability is slightly less absolute. The trade is upside potential for a bit more variability.

The transparency advantage

Level-funded plans give employers claims data and reporting that fully-insured plans rarely do. That visibility lets you actually manage your healthcare spend over time, rather than just absorbing whatever renewal increase the carrier hands you.

Which one fits your group

There's no universal answer. A healthy, stable workforce often does better level-funded; a group with known high claims or one that needs absolute budget certainty may prefer fully-insured. The right call depends on your specific census, risk tolerance, and cash flow — which is exactly the kind of judgment a good advisor exists to provide.

The bottom line

Fully-insured trades upside for simplicity; level-funded trades a little predictability for transparency and refund potential. Neither is universally better. The mistake isn't choosing one — it's choosing without understanding the trade, which is how employers end up overpaying year after year.